The phone rang just after lunch.

The woman on the other end spoke politely.

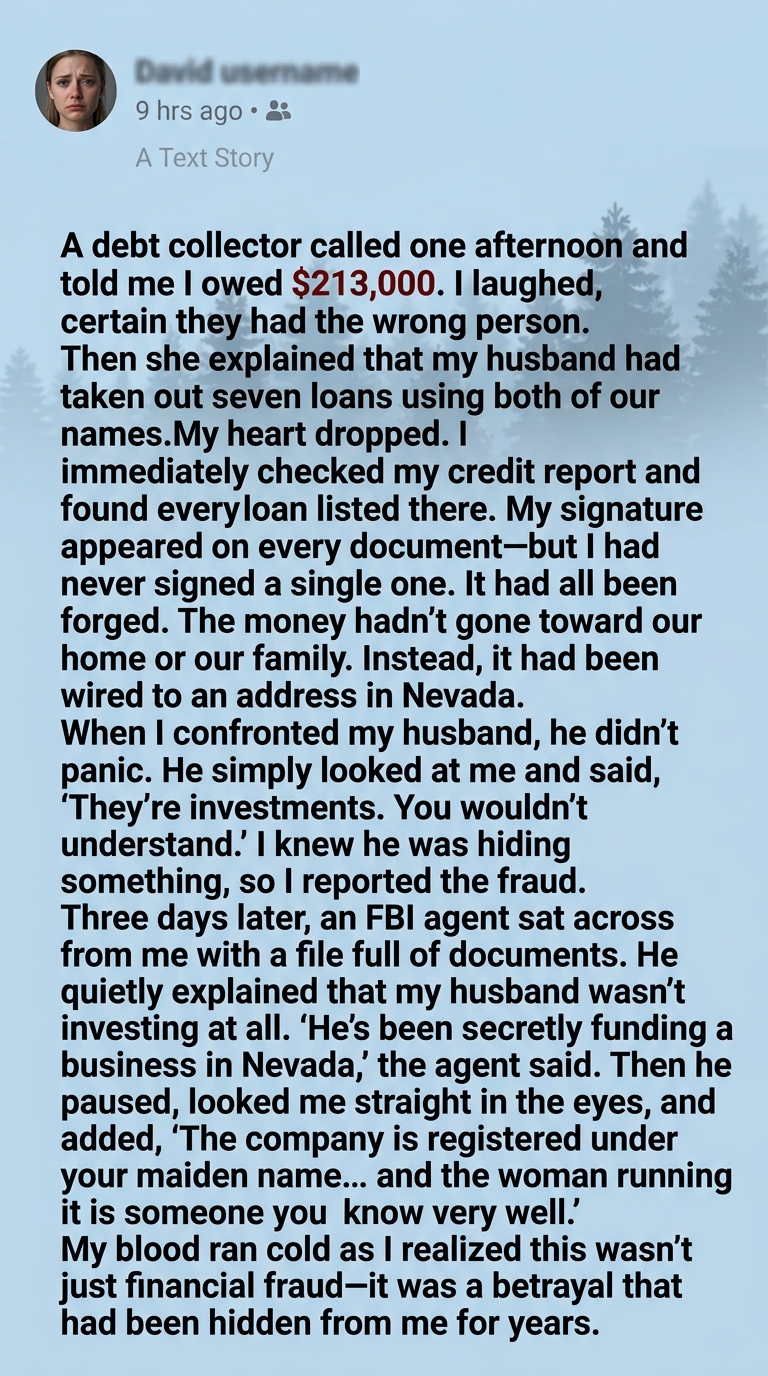

“I’m calling regarding your outstanding balance of two hundred thirteen thousand dollars.”

I actually laughed.

“I’m sorry, but you have the wrong person.”

There was a brief pause.

She confirmed my full name.

My address.

My date of birth.

Then she listed seven separate loans.

Every one of them appeared to have my signature.

My laughter disappeared.

The moment I hung up, I opened my credit report.

There they were.

Seven loans.

Seven forged signatures.

Seven debts I had never agreed to.

My hands shook so badly I could barely hold the mouse.

The money hadn’t gone toward remodeling our home.

It hadn’t paid for medical bills.

It hadn’t funded our children’s education.

According to the loan records, nearly every dollar had been wired to the same address in Nevada.

That evening, I confronted my husband.

He barely looked up from his laptop.

“They’re investments.”

“What investments?”

“You wouldn’t understand.”

“I understand forgery.”

He sighed as though I were the unreasonable one.

“Everything will pay off eventually.”

I stared at him.

“My name is on those loans.”

“We’re married.”

“It’s the same thing.”

“No,” I answered quietly.

“It isn’t.”

The next morning, I contacted my bank, placed fraud alerts on my credit files, and filed reports with the appropriate financial institutions and law enforcement.

Within days, I was contacted by federal investigators because several complaints involving the same lending network were already under review.

An FBI agent sat across from me with a thick file.

He spoke carefully.

“We believe your identity was used without your authorization.”

Then he slid a document across the table.

“The money wasn’t invested the way you were told.”

He pointed to a business registration.

“The company receiving most of the funds is registered under your maiden name.”

I stared at the paperwork.

“That’s impossible.”

“It gets stranger.”

He turned another page.

“The registered manager is someone you know.”

My heart pounded.

Printed on the page was my cousin, Rachel.

We had grown up together.

She had even been a bridesmaid at my wedding.

“There has to be a mistake.”

“I wish there were.”

Investigators explained that the business appeared to exist on paper, but they believed false identity information had been used in parts of its registration.

Using my maiden name had made the paperwork look more legitimate to some lenders, even though I had never authorized it.

When Rachel was interviewed, the truth finally emerged.

Years earlier, she had started a small business that struggled almost immediately.

Instead of shutting it down, she turned to my husband for help.

He secretly began sending her money.

At first, it came from his personal accounts.

When those funds ran out, he applied for loans.

Unable to qualify for larger amounts on his own, he forged my signature.

Rachel admitted she knew he was borrowing money but insisted she believed I had agreed to it.

She was horrified when investigators explained I had never signed anything.

“I asked him over and over if your wife knew,” she said through tears.

“He always said yes.”

My husband eventually admitted what he had done.

“I kept thinking the business would succeed.”

“Then I’d pay everything back before you ever found out.”

“But every new loan only covered the last one.”

What he called investing had become a spiral of deception.

The legal process took many months.

The forged documents were examined.

Financial institutions conducted their own reviews.

Some debts were removed from my responsibility after investigators confirmed the signatures were fraudulent, while other issues were resolved through the courts and the lenders’ established procedures.

My marriage, however, did not survive.

One afternoon, while packing boxes, my husband quietly asked,

“Was it really the money?”

I looked at him.

“No.”

“It was the moment you decided you had the right to sign my name.”

“You didn’t just borrow money.”

“You borrowed my identity.”

He lowered his head.

“I know.”

Months later, my credit was finally restored.

It wasn’t quick.

It wasn’t easy.

But piece by piece, my financial life became my own again.

I also learned something I wish I had understood years earlier.

Love doesn’t require giving someone unlimited access to your trust.

Healthy relationships include honesty, transparency, and respect for each other’s financial independence.

Those aren’t signs of suspicion.

They’re signs of partnership.

Looking back, I realized the biggest debt in my marriage wasn’t the money.

It was the cost of believing that trust could survive when someone quietly signed another person’s name and hoped the truth would never catch up.

By the time the loans disappeared from my credit report, one thing was absolutely clear.

My future no longer carried someone else’s signature.