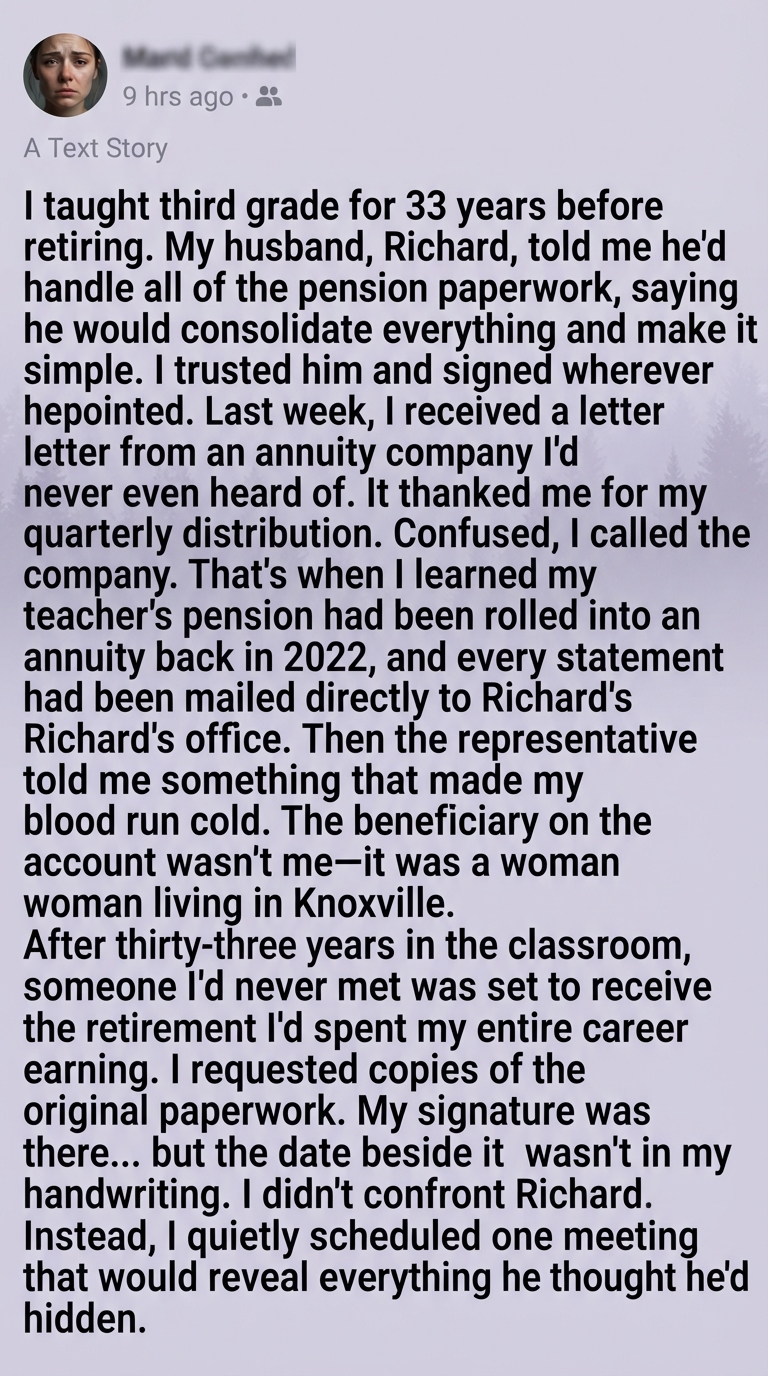

I taught third grade for thirty-three years.

Every September, I welcomed a new group of eight-year-olds into my classroom.

I taught multiplication.

Book reports.

How to write thank-you notes.

How to apologize when you hurt someone’s feelings.

When I retired, I thought the hardest part would be saying goodbye to the children.

I was wrong.

My husband, Richard, insisted he would handle all of my retirement paperwork.

“You’ve spent your whole life taking care of everyone else,” he said.

“Let me take care of this.”

I trusted him.

Whenever a form arrived, he’d place it on the kitchen table.

“Sign here.”

I rarely questioned it.

We had been married for thirty-five years.

Last week, an envelope arrived from an annuity company I didn’t recognize.

The letter thanked me for my quarterly distribution.

Quarterly distribution?

I had no idea what they were talking about.

I called the customer service number.

The representative verified my identity.

Then she explained that my teacher retirement funds had been rolled into an annuity in 2022.

Every statement had been mailed to Richard’s office address.

“I never requested that.”

There was a pause.

Then she said something I’ll never forget.

“The current beneficiary is not you.”

I laughed nervously.

“Of course I’m the beneficiary.”

“I’m sorry, ma’am.”

“The primary beneficiary listed on the account is another individual.”

She gave me the woman’s name.

A woman living in Knoxville.

I’d never heard of her.

I asked for copies of every document associated with the account.

When they arrived, my signature appeared on the transfer paperwork.

But something immediately stood out.

The date written beside my signature wasn’t in my handwriting.

I didn’t accuse Richard.

Not yet.

Instead, I scheduled a meeting with the annuity company, my own attorney, and a financial adviser who specialized in retirement accounts.

I wanted to understand exactly what had happened before saying a word.

During the meeting, the company reviewed the account history.

The transfer itself had been processed using documents that appeared complete at the time.

However, when we compared multiple records, questions emerged about whether every change had been properly authorized.

My attorney requested the original files, signature records, and communication logs.

Several weeks later, we sat down with Richard.

Not alone.

With counsel present.

My attorney calmly placed the documents on the table.

“Can you explain why your wife’s retirement statements were redirected to your office?”

Richard stared at the papers.

No answer.

“Can you explain the beneficiary designation?”

Still nothing.

Finally, he whispered,

“I never meant for her to find out this way.”

The woman in Knoxville wasn’t a secret daughter.

She wasn’t a stranger.

She was Richard’s longtime girlfriend.

Their relationship had begun several years earlier.

He admitted he had changed the mailing address so I wouldn’t see the account statements.

He also acknowledged signing or submitting paperwork that he represented as routine retirement documents.

He insisted he believed he could “fix everything later.”

Instead, he had spent years building a second life.

The legal process that followed was slow and careful.

The annuity company conducted its own internal review.

My attorney helped me dispute transactions and beneficiary changes that I maintained I had not knowingly authorized.

The matter was addressed through the appropriate legal channels, including examination of signatures, account records, and witness testimony.

Eventually, the account was corrected to reflect the proper ownership and beneficiary designation based on the final legal determinations.

My retirement remained mine.

The marriage did not.

Months later, one of my former students visited me.

She was now a teacher herself.

“I still have the note you wrote me in third grade,” she said.

She pulled a folded piece of paper from her purse.

In my own handwriting were the words:

“Always read before you sign.”

We both laughed.

Then I cried.

For years, I’d taught children to pay attention.

To ask questions.

To protect themselves with knowledge.

Somehow, I had forgotten to give myself that same advice.

Looking back, I realized trust isn’t the same thing as giving away your responsibility to understand your own finances.

Partnership means working together.

Not asking one person to sign without knowing.

Now, whenever retired friends ask me for advice about their pensions or investments, I tell them the same thing.

“Read every page.”

“Ask every question.”

“And keep copies of everything.”

Because protecting your future isn’t a sign that you distrust the people you love.

It’s a way of honoring the years you worked to build it.

After thirty-three years in the classroom, my greatest lesson wasn’t one I taught my students.

It was one I finally learned myself.